BUSINESS NEWS - As a long term investor, you cannot avoid taking risk. In order to grow your money meaningfully ahead of inflation over many years, you have to be exposed to markets that are inherently volatile.

In the short term, this means there is a risk that your investments could lose value. Over the long term, however, that volatility is what gives you the opportunity to earn significant returns.

The only risk-free investment is putting your money in the bank. This might ensure that you never lose any of it, but over the long term, this will not give you much real growth.

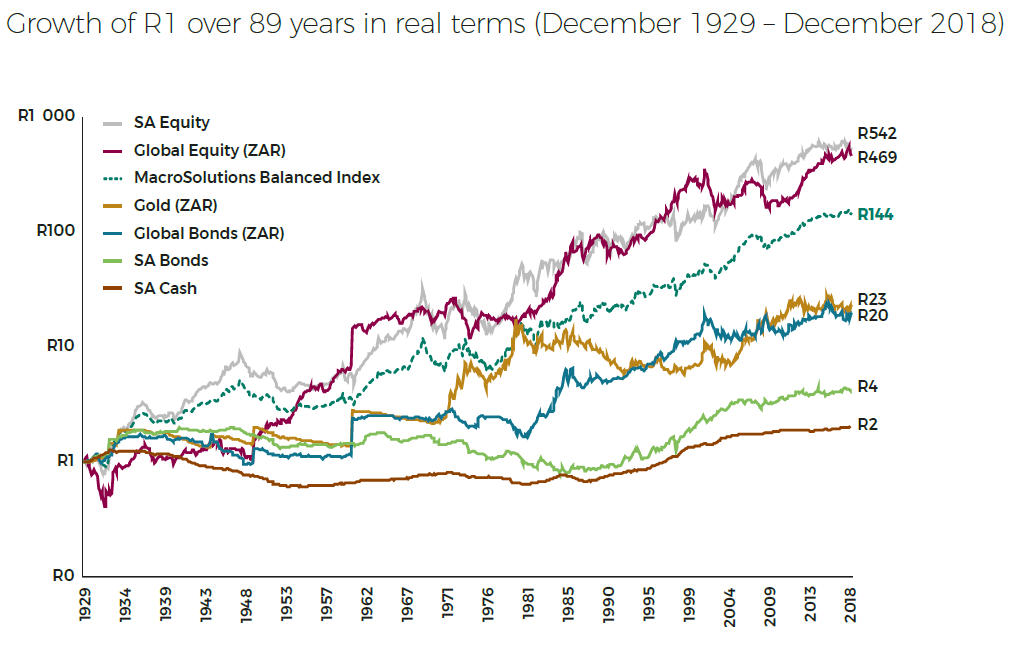

As the graph below illustrates, R1 invested in cash over 89 years would only have grown to be worth the equivalent of R2 in 1929 money. The same rand invested in the local stock market would have grown to be worth the equivalent of 270 times more.

Source: Old Mutual MacroSolutions

It is worth noting that this graph starts with the Great Depression. For the first three years of this time frame, cash in the bank would have significantly outperformed any stock market investment. It would have seemed like an incredibly good idea at the time to avoid shares.

Within just a few years, however, stocks would already have delivered massive outperformance and that would have continued to be the case ever since.

The silent killer

There are two significant factors at play here. The first is the biggest risk that many investors fail to recognise.

Over the long term, the greatest risk to your wealth is not the volatility of the stock market or downgrades to South Africa’s credit rating. It is that you fail to insure yourself against the silent threat to your money – inflation.

You may feel secure that the R100 you put in the bank last year is still R100 today, but that would be ignoring the fact that it is no longer has the same value … R100 today is not worth the same as R100 was 12 months ago.

You can no longer buy as much with that same money.

At an inflation rate of around 4.5%, your R100 would now be worth the equivalent of R95.50. And this decrease in value compounds over time. Your money progressively becomes worth less and less, unless you invest it in a way that it will grow ahead of inflation.

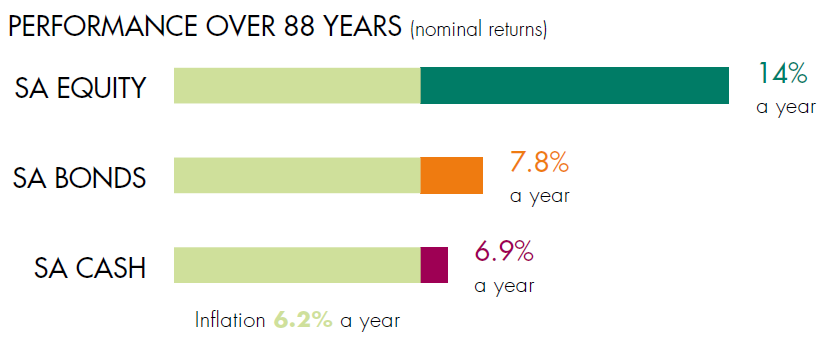

That requires you to take the short term risk that comes with investing in the stock market, because over the long term you can’t afford not to. As the below graphic illustrates, cash has historically only just beaten inflation in South Africa. In the stock market, however, investors have seen meaningful real returns.

Source: Old Mutual MacroSolutions (to December 2017)

There is no substitute for time

The second vital consideration is that the benefits of being invested in the stock market do not play out over a few years. On the contrary, investing in shares can often seem like a pretty bad idea. The Great Depression is an obviously example of this, but the JSE’s performance since 2014 is another.

Over the last five years, the local market has only beaten inflation by around 1.5%, and has underperformed cash. On that performance there would appear to be little to recommend it.

Since 1924, however, the JSE has gone up in a calendar year more than twice as often as it has been negative. In 64 of those years, the market has shown a positive return – and it has only gone backwards in 31.

In fact, the local stock market has delivered a return of more than 10% in a calendar year more often than a negative one. What this means is that, over the long term, returns from the stock market actually become fairly reliable.

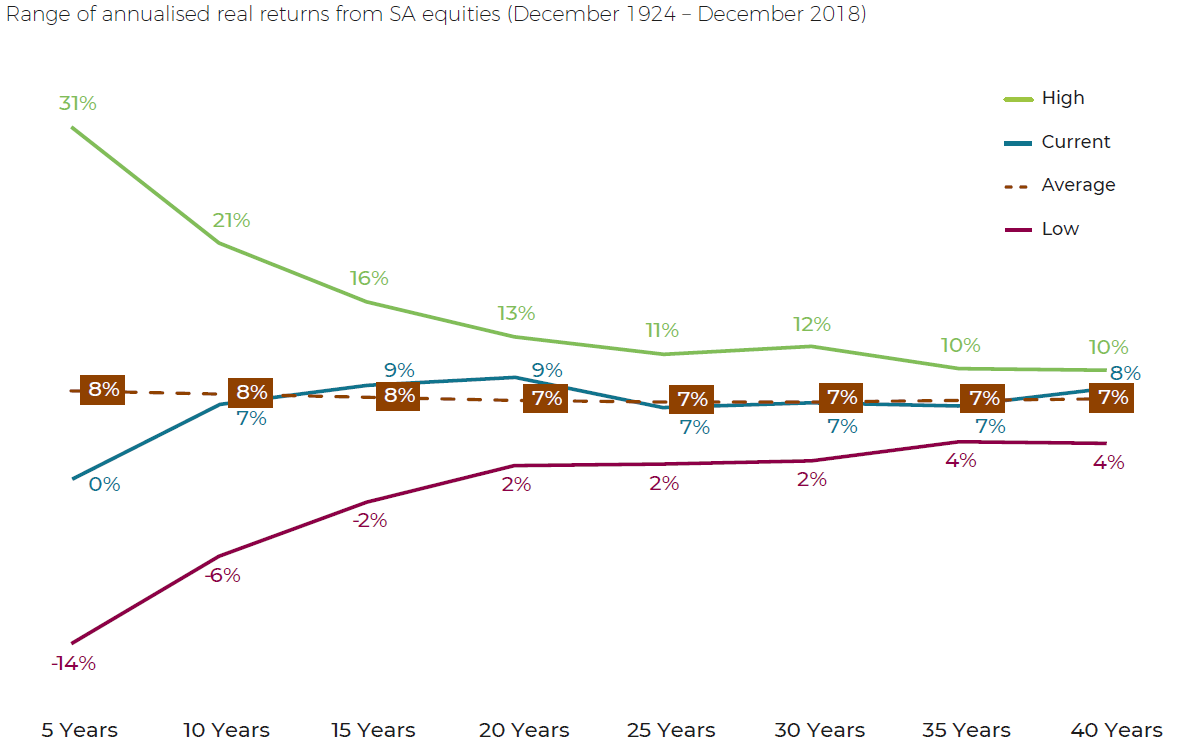

The below graph illustrates the best and worst real return (after inflation is taken into account) from the stock market over a range of periods from 1924 to the end of 2018. At that point, the JSE had not beaten inflation for five years. Yet any investor whose time horizon was at least 20 years had never seen their money lose value.

Source: Old Mutual MacroSolutions

Significantly, given a time frame of 20 years or longer, JSE returns have been in a fairly narrow, and predictable band.

On average, investors who kept their money in the stock market for at least two decades have seen their wealth grow at 7% above inflation.

Nobody can guarantee that this will continue to be the case, but history has been a reliable guide. Even in the current environment, returns have fitted well within the long term pattern.

This is an important consideration for long term investors. The value of the stock market – whether locally or globally – has been proven over time. Underperformance in the short term needs to be seen in that context.